The interaction between onshore and offshore RMB Markets

Abstract

The RMB has grown in importance as a global currency, with both onshore and offshore markets playing a vital role for Chinese economy.

Based on previous literature, that investigated the relation between CHN and CYN and the internalisation of the currency, this paper explores the interaction between these two markets, through a quantitative and qualitative approach.

Analysing the interconnection between CNY and CHN through average comparison, the variance percentage and the correlation analysis and through events, such as the exchange reform of 2015 and Covid-19 crisis, is possible to understand the various trend of Chinese financial market.

In conclusion, as the RMB continues to internationalise, these interactions are expected to evolve, impacting global trade and investment. Consequently, understanding the interaction between onshore and offshore RMB markets is vital for policymakers, investors, and businesses engaging with China.

Background

The Internalisation of RMB is a process characterised by different steps, but to have a comprehensive understanding of it, there is the necessity to provide a definition. The internalisation of the RMB means getting RMB outside of China and consenting people, who are not residents in China, to bring RMB overseas and use it as a currency for routine payments, settlements, investments and reserves.

The Chinese economy has two faces, namely two distinct markets: the onshore market, also known as the CNY market and the offshore market, or CNH market.

The CNY is administered by the People’s Bank of China or China central bank. The Chinese government has a strict control of the CNY rate on the mainland, in fact the currency can trade within a limit capacity of 2% over or under the rate of the day. If there is a far differentiation from this percentage, the central bank has to cover the daily volatility, buying or selling the yuan. The PBOC, which is influenced by the central government, decides the daily reference rate, to direct the market and to guide the currency. These practices have the objective to strengthen and preserve an advantage for Chinese economy.

The CNH is the currency that’s traded offshore from Mainland China. Before 2004, the currency was diffused out of China without any kind of regulation. In the same year, banks in Hong Kong started to take deposits, accepting exchanges and remittances.

In 2007, the currency reached the capital investment level with the birth of Dim Sum Bond, which refers to Mainland banks started to issue RMB bonds in Hong Kong. In fact, at the beginning, the Chinese coin started trading only in Hong Kong, and then it has expanded worldwide. For this reason, the letter “H” was initially referred to Hong Kong as the first offshore market for the currency.

After the outbreak of the global financial crisis, the Chinese government was concerned about defaults due to U.S. inflation and regarding the safety of China’s U.S. dollar assets. Consequently, two ideas emerged to reconstruct the essential monetary system. One suggested a progressive shift away from the U.S dollar adoption of the Special Drawing Right (SDR) as the primary international reserve. The alternative proposal addressed for the incorporation of new regional currencies, such as the Asian yuan, through local financial collaboration and a multipolar monetary system, encompassing the euro and the U.S. dollar as the primary international reserve currencies, namely setting limits on the dominance of the dollar.

These two reforms did not work as expected, consequently China decided to undertake the path of internationalisation, with the objective to make the RMB equal to the U.S dollar and Euro.

A Pilot program, that increased the quantity of RMB overseas, started in 2009, when a huge number of enterprises in different Chinese cities initiated cross-border currency deal settlements with Hong Kong, Macau, Taiwan and ASEAN countries and the year after this program was enlarged to 20 provinces in all Countries. The cross-border business had reached an impressive development since its birth, from “less than 3.6 billion yuan in 2009 to 2.08 trillion yuan in 2011”. In 2011, China announced several measures to push RMB internationalisation, because the aim of CNH is to internationalise the currency.

Chinese currency is tightly linked to political reforms that the government has improved during these years. The most important reform is the exchange rate system. In 2015, the reform implemented by People-s Bank of China, marked a significant shift in China-s approach to managing its currency. The aim was to make the currency exchange rate more market-oriented and responsive to supply and demand forces, moving away from previous peg to the U.S dollar. In 2018, to fight against the tariffs imposed by the US, during trade war, China decided to depreciate the currency. Nowadays the exchange rate is allowed to float more widely than before on a daily basis.

A series of reforms have been implemented to internationalise the currency. For instance exporters are now allowed to make use of the Chinese yuan for pricing and settlement; companies are able to employ the RMB in cross-border direct investment; foreign governments an financial institutions are now authorised to obtain and preserve Chinese government bonds; interest rate can be determined by supply and demand in the market and foreign investors can take part in China’s stock and bond markets, although with restrictions.

The aim of China of being a global economy could be reached connecting CNH and CNY markets. Although these two markets are interrelated and moved freely from onshore to offshore, they are managed by different ways, and this can affect negatively their interaction.

Literature review

The analysis of this paper is based on different studies that investigate the interaction between CNY and CNH and reveals several key aspects of this relation.

The paper of Shuairu Tian, Xiang GAO and Xiaojing Cai (2023) is focused on the interaction between CNY-CNH in the time of 2010-2022. Through wavelet methodology, they found that the relationship between these markets is bi-directional and asymmetric. This relation is time-varying, with differences in reaction to the frequency and strengthened by events such as Exchange rate reform, the US-China war and Covid-19.

Jing Qin (2019) studied the interaction between CNY and CNH market with a specific focus on the exchange rate reform’s influence in August 2015. The results demonstrated that in this relationship exists clear capacity law through correlations by the influence of interest rate, US currency and the Reform, that affecting the different scale through correlation coefficient curves. Moreover, this research supported the idea that when there is a huge shock, the risk of offshore RMB markets in Europe and the UK is bigger than in Hong Kong and US.

Genhua Hu, Xiangjin Wang and Hong Qiu (2023), focus on the relation of dependence between RMB exchange rates in the offshore and onshore market during extreme market conditions. They use correlation multivariate volatility Copula and BEEK models. Through these means, they observe that there is a necessity to formulate risk diversification policies by describing the interconnection characteristics of conditions between RMB exchange rate markets inside and outside the country. The interaction is time-varying and non-linear between the RMB exchange rate in onshore and offshore markets as well as volatility spillover phenomenon, which indicates a reliance relationship of dynamic conditions between different currency exchange rate markets.

In Sercan Eraslan studies (2017), there is a highlight on the effects of arbitrage trading. This phenomenon is affected by market regulation, the size of onshore and offshore, pricing differential and appreciation-depreciation trends. For instance, during times in which arbitrage trading was missing, dynamics of RMB rates were influenced by general global risk and global liquidity.

Samar Maziad and Joon Shik Kang (2012) also investigated policy implications on the interaction between RMB onshore and offshore markets. They suggested that supportive policies are important to ensure a evolution of RMB’s role, that could increase assets offshore, improved financial system, raised freedom of movement and build the RMB’s trustworthiness.

Based on this literature, this paper has explored the interaction between onshore and offshore RMB markets, focusing on average comparison, variance percentage and correlation analysis based on data provided. Moreover, the research has investigated key events such as exchange rate reform of 2015 and Covid-19 crisis, that affect the relationship between onshore and offshore RMB markets.

Analysis and Interpretation

This paper has explored the interaction between onshore and offshore RMB Markets, using a quantitative and qualitative approach.

The data is analysed through Excel data analysis and to measure the interconnection between CNY and CNH are used the average comparison, the variance percentage and the correlation analysis.

Through a qualitative approach, this paper analysed key parameters such as the exchange rate reform of 2015 and Covid-19 crisis, to see how these events affect the relationship.

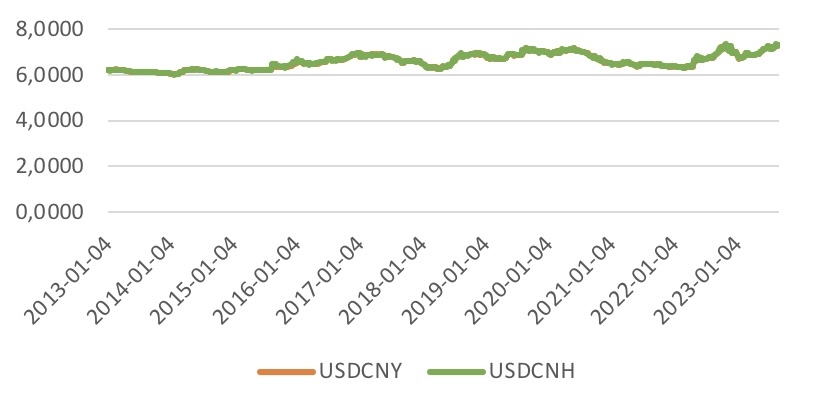

This paper has started to analyse the historical performance of the currency from 2013 until 2023 to show how the relationship between CNY and CNH has been during the years. Calculating the average of data, it is possible to see that the performance of each currency is similar, in fact the average for USD/CNY is 6,590 while the average for the USD/CHN is 6,595. Consequently, the trend of both currencies is almost overlapping, and it is also demonstrated by the minimum difference between the averages, that is 0,0047. Some exceptions are visible on the graph, and they are due to exchange rate reform of 2015, trade war of US-China and global crisis, such as Covid-19.

USDCNY | USDCNH | |

Average | 6,590126312 | 6,594813617 |

Difference | -0,004687305 | |

After this first analysis, it is possible to investigate the interaction between CNY and CNH currencies, through a variance percentage. This calculation is the difference between the old number and the new one, divided by the first one and multiplied for one hundred. In this case, the result shows again that there is a close interaction, and this idea is also supported by the graph. The variance is near to zero (0,08), for this reason the relation demonstrates that there always was the will to link these two markets, with the aim to reach the position of global economy by China. In fact, this relation is influenced by the presence of the government that wants to achieve the goal to have the same path for both currencies, through the implementation of different policies and the imposition of a limited capacity for trade.

The analysis proceeded through the correlation analysis that was done through the historical performance of the currencies, CNY and CNH, using the function of correlation coefficient in the Excel data analysis. This method is useful to demonstrate if there is a relationship between two variables. The values can be from “-1” to “1”. The first one regards negative relations, the second one concerns positive correlations.

Based on data, it is observable that the correlation coefficient is 0,998, namely very close to 1. Consequently, there is a positive correlation between the two currencies and they both are dependent on each other. In fact, also through the graph, it is possible to understand that CNH follows the flow of CNY, and it is influenced by the choices of the government. The currencies are going through the identical direction with the same goal, namely bringing China to be the world’s largest market economy.

The analysis of the paper continues to explore the relation between the currencies through two events.

The first one is the Reform of 2015 regarding the daily fixing of the RMB. The main objective of this reform was to strengthen the currency against the US dollar and improve the affection of the market and that of major currency movements. Thanks to it, it was possible to end the gap between the market value and the fix.

As a result, mainly at the beginning, this change influenced the relation between CNY and CNH. In fact, as it is shown on the graph, each path did not follow the same direction. There was a CNH appreciation that coincided with a spike in CNH interest rates. Consequently, the CNH was squeezed by the central bank to limit the gap between both currencies. The same situation happened in January 2016, when CNH was dealt at a depreciate rate level in relation to the CNY.

After this reform, the offshore CNY market has lost its role as the pricing head of the exchange rate of RMB, which it is in favour of, as well as the affection of the offshore CNH on CNY has increased. Despite it, co-movement of the currencies’ path continued thanks to the counter cyclical adjustment (McCauley, R. N., & Shu, C., 2017), in which “the depreciation of the exchange rate during a day should not necessarily be validated by incorporation in the next fixing if the economic fundamentals do not warrant it.”

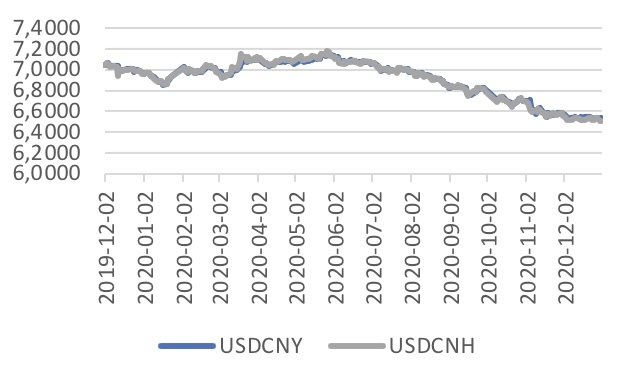

The second one is the Covid-19 crisis, that caused a strong fluctuation in the renminbi exchange rates during the period from December 2019 until the end of 2020. The depreciation trend until May 2020 was followed by a rapid appreciation. This situation was due to the sensitiveness of the foreign exchange market and its financial risk infection that transmitted the CNY exchange rate fluctuation on the offshore market.

During Covid-19 period, the volatility spillovers between the currencies have increased and also as shown on the graph, there was discrepancy. This can be caused by the fact that the CNH market is more responsive to international market and global economic conditions, consequently during times of crises, the offshore market may reflect a different set of factors. Moreover, during periods of uncertainty, the probability to have divergence in rates between the onshore and offshore market is higher due to market dynamics, capital flows and market sentiment.

Conclusion

The interaction between onshore and offshore RMB markets is a dynamic process with implications for both the Chinese economy and the global financial system.

This study has shown the interaction between these markets, starting from the background that highlights the internalisation process and the characteristics of the onshore and offshore markets.

Thanks to the literature, it was possible to underscore the complexity of the CNY-CNH relationship. Notable findings include the bi-directional and asymmetric information spillover between the currencies, the impact of policy reforms, and the risk during extreme market conditions. Based on these researches, this paper was able to study the interaction between CNY and CNH markets and contribute to this body of knowledge.

The quantitative and qualitative analysis undertaken in this paper emphasises the correlation between CNY and CNH. Historical performance analysis, average comparison, variance percentage and correlation coefficient calculations consistently indicate a positive and strong relationship. This alignment is given by China’s strategic goal of becoming a global economic, and it’s reflected in the government’s influence on both markets.

Moreover, the paper focused on the study of the influence of events, such as exchange rate reform of 2015 and the Covid-19 crisis. These events reveal how the currencies respond to external shocks and government intervention. Despite some nuanced interactions, they are strongly connected, and they both affect each other. In summary, this paper contributes to the understanding of the onshore and offshore RMB market relationship, confirming the positive interaction that can be defined as“bidirectional” and “asymmetrical”. They can move from onshore market to offshore market and vice versa, but they are controlled in a different way.

As the RMB continues to internationalise, these interactions are expected to evolve, impacting global trade and investment.

Understanding the interaction between onshore and offshore RMB markets is vital for policymakers, investors, and businesses engaging with China. Further research is needed to explore the evolving nature of this interaction and its consequences for the broader financial landscape.

References

Eraslan, S. (2017) Asymmetric arbitrage trading on offshore and onshore renminbi markets, SSRN. Available at: https://deliverypdf.ssrn.com/d... (Accessed: 30 November 2023).

Feng, Y. and Tang, Y. (2016) The dynamic relationship between onshore and offshore ... - atlantis press. Available at: https://www.atlantis-press.com... (Accessed: 30 November 2023).

Genhua Hu a b et al. (2023) Analyzing a dynamic relation between RMB exchange rate onshore and offshore during the extreme market conditions, International Review of Economics & Finance. Available at: https://www.sciencedirect.com/... (Accessed: 30 November 2023).

Jing Qin et al. (2019) Relationship between onshore and offshore renminbi exchange markets: Evidence from multiscale cross-correlation and nonlinear causal effect analyses, Physica A: Statistical Mechanics and its Applications. Available at: https://www.sciencedirect.com/... (Accessed: 30 November 2023).

Labonte , M. and Morrison, W. (2013) China’s currency policy: An analysis of the economic issues - CRS reports. Available at: https://crsreports.congress.go... (Accessed: 30 November 2023).

Maziad, S. and Kang, J.S. (2012) RMB internationalization: Onshore/offshore links - IMF. Available at: https://www.imf.org/external/p... (Accessed: 30 November 2023).

McCauley, R. and Shu, C. (2018) BIS working papers - Bank for International Settlements. Available at: https://www.bis.org/publ/work7... (Accessed: 30 November 2023).

Renminbi internationalization: Background and milestones (2017) CFA Institute Enterprising Investor. Available at: https://blogs.cfainstitute.org... (Accessed: 30 November 2023).

Sahelirc (2019) The yuan hit an 11-year low this week. here’s a look at how China controls its currency, CNBC. Available at: https://www.cnbc.com/2019/08/2... (Accessed: 30 November 2023).

Shuairu Tian a et al. (2023) The interactive CNY-CNH Relationship: A wavelet analysis, Journal of International Money and Finance. Available at: https://www.sciencedirect.com/... (Accessed: 30 November 2023).

Sun, R. and Park, C. (2021) Interactions between the exchange rate of RMB/USD in the onshore and ... Available at: https://agbioforum.org/sobiad.... (Accessed: 30 November 2023).

Wang, L., Xiong, X. and Cao, Z. (2023) Time-frequency volatility spillovers between Chinese renminbi onshore and offshore markets during the COVID-19 crisis, Nature News. Available at: https://www.nature.com/article... (Accessed: 30 November 2023).

Wong, A. (2023) CNH vs CNY: Comparing the two chinese RMB currencies: Airwallex HK, CNH vs CNY: Comparing the Two Chinese RMB Currencies | Airwallex HK. Available at: https://www.airwallex.com/hk/blog/cnh-vs-cny-the-differences-in-chinese-renminbi# (Accessed: 30 November 2023).

Zhang, M. (2015) Developments, problems and influences - cigionline.org. Available at: https://www.cigionline.org/sta... (Accessed: 30 November 2023).